.svg)

Minnesota’s PPP/EIDL suspensions are a real-time case study in how “post-program enforcement” works, and why advisors should move ERC clients into audit defense before the next wave hits.

Run an ERC Defense Readiness Review

Built for CPAs, banks and financial professionals managing ERC exposure at scale.

In early January 2026, the SBA announced it had suspended 6,900 Minnesota borrowers tied to 7,900 PPP and COVID EIDL loans totaling roughly $400 million, restricting access to new SBA lending as part of a broader PPP investigation while suspected loan fraud is reviewed.

SBA Administrator Kelly Loeffler described Minnesota as “just the first state,” reinforcing that this is being framed as the start of a broader cleanup posture, not an isolated event.

How PPP, EIDL, and ERC Converge in the Scrutiny Era

PPP (Paycheck Protection Program)

EIDL (Economic Injury Disaster Loan)

ERC (Employee Retention Credit)

Different agencies, different mechanics, but the enforcement reality converges in audit IRS terms because all three:

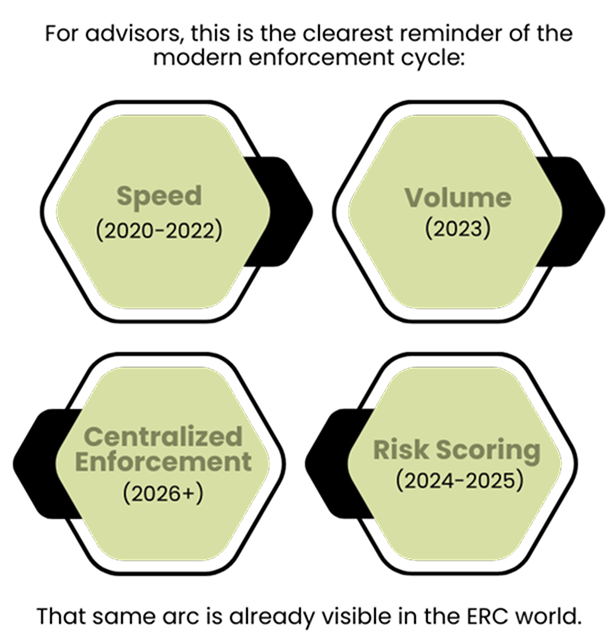

The IRS has already signaled that ERC is past the “filing gold rush” and deep into enforcement and correction.

In other words, Minnesota isn’t “about PPP.” It’s about posture. And that posture is already here for ERC.

Minnesota, effectively a live PPP loan investigation case study, illustrates three patterns advisors should expect to see repeated across other COVID-era programs:

The SBA didn’t target one borrower; it flagged thousands at once.

That’s the model: centralized analytics → mass screening → escalations.

The enforcement tool wasn’t only “investigate.” It was “restrict future eligibility while we investigate.”

When an agency believes a market got flooded with aggressive activity, they look at the ecosystem: preparers, promoters, brokers and patterns. (That’s been explicit in ERC enforcement messaging.)

Payroll providers are targets, even when they do everything “right.”

They’re often the operational backbone that processes payroll filings and supports ERC submissions. But that creates a catch-22:

This is why payroll teams should treat ERC as a relationship and reputational risk, not just a tax topic.

Harbor Shield ERC is an additional layer clients can adopt so that if questions come later, they’re not forcing the payroll provider to be the defender. It helps payroll firms say:

“We can support you operationally, but you should also have a dedicated defense plan in place for ERC-specific scrutiny.”

Add a Defense Layer for Your ERC Filers

A lot of financial institutions supported ERC education and promotion. Many also refused to engage with certain ERC approaches entirely.

That creates two very real client segments for banks (and both are valuable):

These clients may now want an added layer of protection as scrutiny increases. The bank can proactively offer a prudent next step.

These clients are the ones most likely to come back under stress later. The bank needs a nonjudgmental way to say:

“Regardless of how you got there, here’s what you should do now to protect yourself.”

Most clients think ERC audit risk is binary:

“Will they make me pay it back?”

But in practice, what hits first is often:

That’s why the smartest advisory move is separating:

What’s happening in Minnesota makes this easier to explain: even before guilt is proven, access can be restricted and cases can be reviewed at scale.

Harbor Shield ERC is positioned as the risk transfer layer for clients who have already claimed ERC and want to avoid the “scramble and pay whatever it takes” moment later.

The advisor framing is simple:

Minnesota isn't a one-off; it's a preview. As the focus shifts to rooting out a few bad actors, the burden of proof falls on the group. The smartest move is to secure defense capacity now, while you still have the time to act deliberately.

See How Harbor Shield ERC Works for Advisors

Compliance notes: This article is for educational and operational overview purposes only and does not constitute tax or audit legal advice. You should consult qualified tax and legal professionals regarding your specific facts and circumstances.

.svg)

.svg)

.svg)

.svg)

.png)